Book Value Definition Ifrs

Ifrs Meaning Objectives Assumptions And More In 2020 Financial Statement Financial Management Accounting Books

Ifrs 13 Fair Value Measurement In 2020 Fair Value Financial Asset Financial Accounting

Https Www Sapspot Com Depreciation To The Day Functionality In 2020 Day Life Cycles Book Value

Ifrs13liabilities In 2020 Being Used Quotes Fair Value Financial Instrument

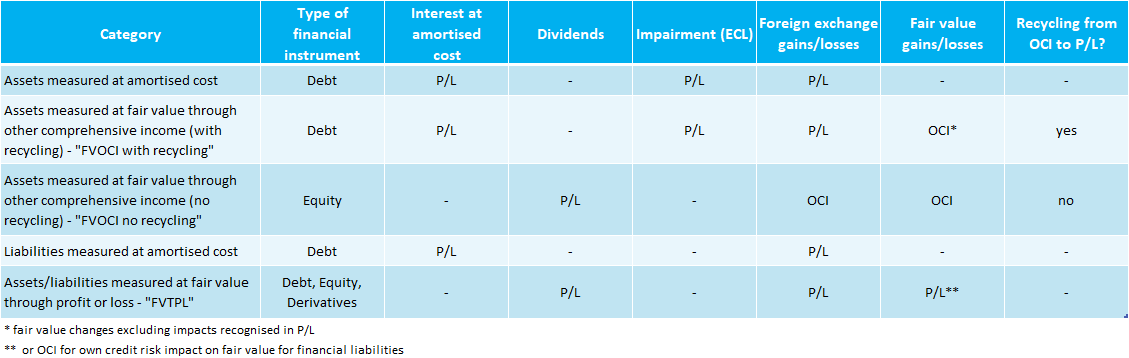

Measurement Of Financial Instruments Ifrs 9 Ifrscommunity Com

It is determined as the cost paid for acquiring an asset minus any depreciation amortization or impairment costs applicable to the asset.

Book value definition ifrs. Book value is calculated by subtracting any accumulated depreciation from an asset s purchase price or historical cost. Book value or carrying value is the net worth of an asset that is recorded on the balance sheet. It s wise for investors and traders to pay close attention however to the nature of the company and other assets that may not be well represented in the book value.

Book value is a widely used financial metric to determine a company s value and to ascertain whether its stock price is over or under appreciated. Book value also known as carrying value or net asset value is the value of an asset that is recognized on the balance sheet. Book value represents the value of assets and liabilities at the date they are reported in a company s documents.

Written down value is the value of an asset after accounting for depreciation or amortization. Book value is equal to the cost of carrying an asset on a company s balance sheet and firms calculate it netting the asset against its accumulated depreciation. For most assets and liabilities book values are based on the historic cost of items.

New Ifrs 13 Fair Value Measurment

Ifrs And Us Gaap A Comprehensive Comparison Steve E Shamrock Financial Health Ebook Buch

Ifrs 13 International Financial Reporting Standards Fair Value Ifrs 2 Ias 17 Png 1949x756px Fair Value

Example Lease Accounting Under Ifrs 16 Youtube

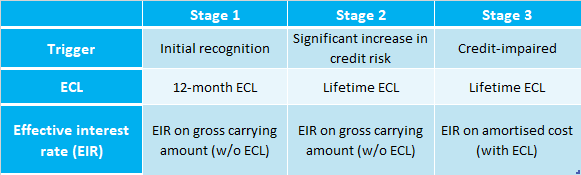

Impairment Of Financial Assets Ifrs 9 Ifrscommunity Com

Management Accounting Financial Management Accounting Managerial Accounting

Ifrs 16 Leases Pkf United Arab Emirates

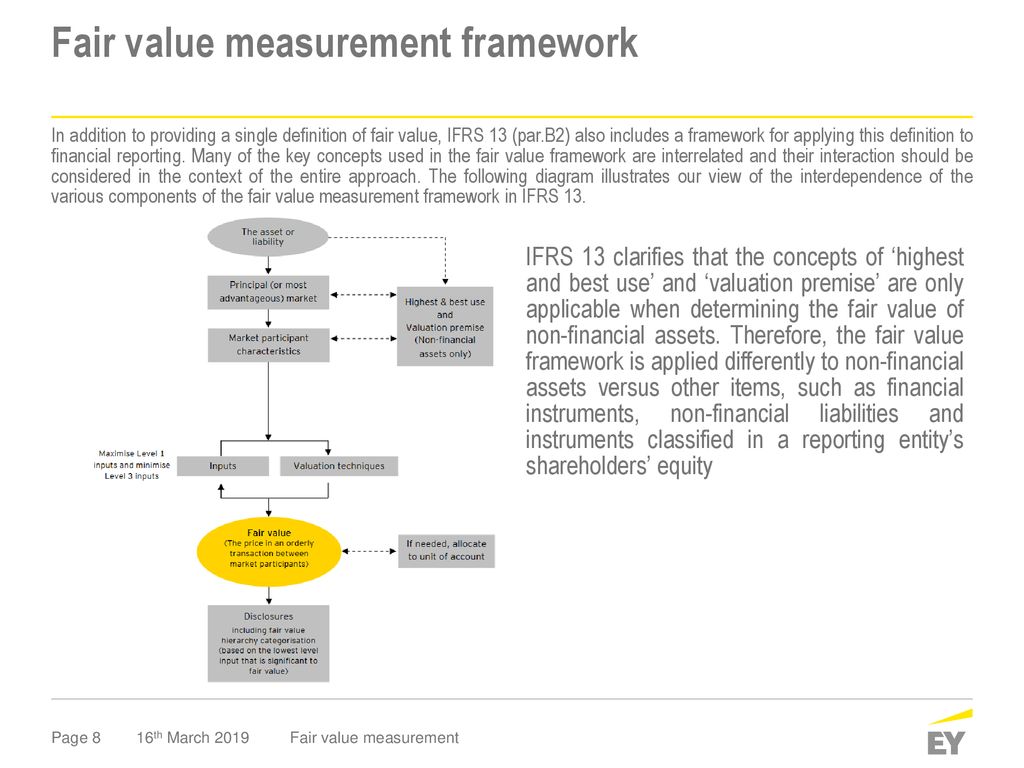

Fair Value Measurement Ppt Download

Infographic Understanding Ifrs 9 For Retail Lending Infographic Understanding Data Mining

Pin On Solution Manual Download

How The Lease Accounting Changes With The New Standard Ifrs 16 Leases See The Comparison With I Hobby Lobby Christmas Hobbies For Kids Hobbies That Make Money

Pdf The Relative Value Relevance Of U S Gaap And Ifrs

Financial Assets Under Ifrs 9 The Basis For Classification Has Changed Bdo Australia